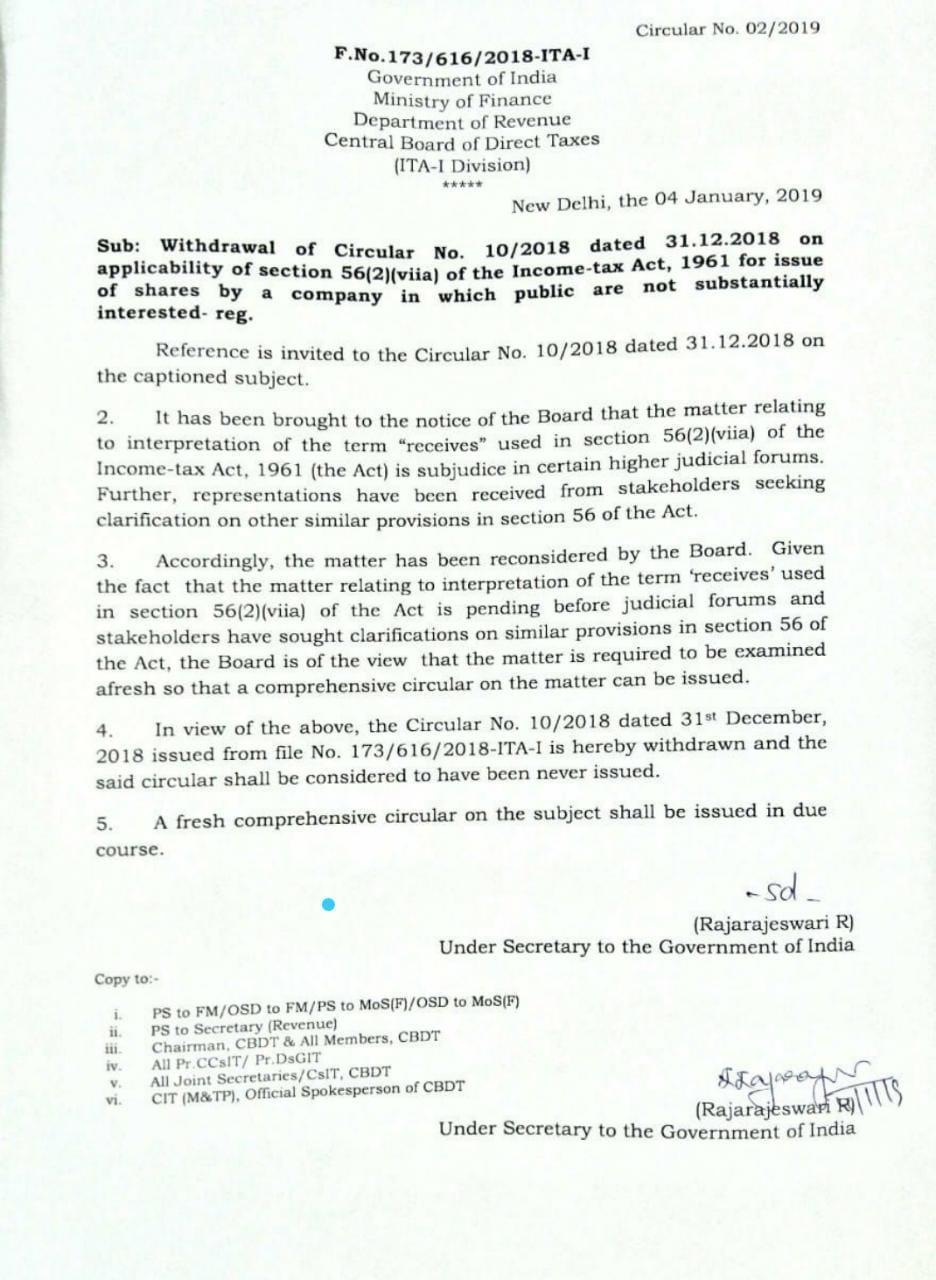

CBDT withdraws Circular no. 10 dated 31st Dec 2018 clarifying that Section 56(2)(viia) of the Income-tax Act, 1961 (‘the Act’) shall not be applicable in cases of receipt of shares by a closely held company (specified company) or a firm as a result of fresh issuance of shares.

Upon reconsideration of the matter, CBDT states that the term ‘receives’ used in Section 56(2)(viia) of the Act is pending before judicial forums and stakeholders have sought clarifications on similar provisions in Section 56 of the Act. Accordingly, CBDT states that “the matter is required to be examined afresh so that a comprehensive circular on the matter can be issued.” Thus, withdrawing the aforesaid circular, CBDT clarifies that “the said circular shall be considered to have been never issued.”

To read more refer CBDT Circular 2/2019 dated 4th Jan 2019 – Click Here

{kind=link}